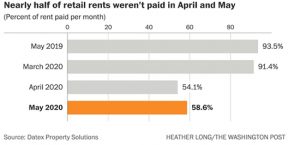

According to the Mortgage Brokers Association under 40% of commercial property, loans are from banks. The majority of loans are in real estate investment (REIT) trusts or commercial mortgage-backed securities (CMBS). CMBS are popular because they mitigate risk by packaging together commercial mortgages. The downside is it adds many layers to ownership. When the investors of a CMBS take ownership of a property they typically use a special servicer who has little incentive to offer any leniency in payment structure. Without conciliation, many renters would be in a position to default and foreclose. In the retail market alone 58.6% of tenants were unable to pay their rents.

Investors are opportunistic about the retail industry with a 2.29% jump in delinquency rate on mortgage loans in April. According to New York-based Trepp Research’s CMBS Delinquency Rate, which measures mortgage payments that are late for more than 30 days. Companies like Blackstone, Starwood, and Oaktree have stockpiled billions of funds for this distressed commercial market. The hope is to follow a playbook similar to 2008 when real estate funds were able to profit by finding extremely discounted properties and ride out the recovery.

For distressed buyers the question remains is the market at an all-time low? When will the market recover? How to determine capitalization rates when you are unsure the tenants will be able to pay their rent? And what are the costs and risks of meeting consumer’s societal and health concerns?